How To Generate A Registered Bonded Bill Of Exchange

Imports and exports are one of the main aspects of an economy as it determines the volume of foreign exchange earnings.

While we discuss the movement of goods, we should also focus on goods being moved in the process of importation and exportation and the e-way bill requirement for the same.

E-way bill is mandatory for inter-state movement of goods of value above Rs 50,000 and for all intra-state movements with further relaxations.

Latest Updates

29th August 2021

From 1st May 2021 to 18th August 2021, the taxpayers will not face blocking of e-way bills for non-filing of GSTR-1 or GSTR-3B (two months or more for monthly filer and one quarter or more for QRMP taxpayers) for March 2021 to May 2021.

4th August 2021

Blocking of e-way bills due to non-filing of GSTR-3B resumes from 15th August 2021.

1st June 2021

1. The e-way bill portal, in its release notes, has clarified that a suspended GSTIN cannot generate an e-way bill. However, a suspended GSTIN as a recipient or as a transporter can get a generated e-way bill.

2. the mode of transport 'Ship' has now been updated to 'Ship/Road cum Ship' so that the user can enter a vehicle number where goods are initially moved by road and a bill of lading number and date for movement by ship. This will help in availing the ODC benefits for movement using ships and facilitate the updating of vehicle details as and when moved on road.

18th May 2021

The CBIC in Notification 15/2021-Central Tax has notified that the blocking of GSTINs for e-Way Bill generation is now considered only for the defaulting supplier's GSTIN and not for the defaulting recipient or the transporter's GSTIN.

What does the term import and export include under the GST Act?

As per the GST Act, import and export are understood in simple terms. Import of goods means bringing goods to India from a place outside India while export means taking goods from India to a place outside India. Further, import of goods as per the IGST Law will be treated as an inter-state supply and IGST will be levied on it. Export of goods will be considered as a zero-rated supply and no tax will be levied on it.

What is the applicability of e-way bill on import and export transactions?

While we just discussed that import is considered to be an inter-state transaction and we know that e-way bill is applicable on inter-state transaction, let us examine the applicability of the same and when one must generate e-way bill under each situation:

A typical import procedure has the following stages:

A- Goods are said to have been imported into India when they reach the port/ airport.

B- on reaching the port/ airport, the goods are under the custody of the customs department and are further transported to an Inland Container Depot (ICD) or a Container Freight Station (CFS) for clearance. This transportation i.e. transportation as per B above is exempted from the requirement of generating an e-way bill under rule 138.

C- from the ICD or CFS, the bill of entry is filed, customs duty is paid by the importer and the goods are cleared for home consumption (eg. place of business like factory or warehouse of the importer). This transportation at 'C' requires an e-way bill. OR

D- the goods can also be kept in a bonded warehouse until it is cleared for home consumption. The transportation of goods as per 'D' i.e. from ICD to the bonded warehouse is exempt from the requirement of carrying an e-way bill. But when the goods are cleared from the bonded warehouse at a future date to the factory of the importer, an e-way bill must be generated.

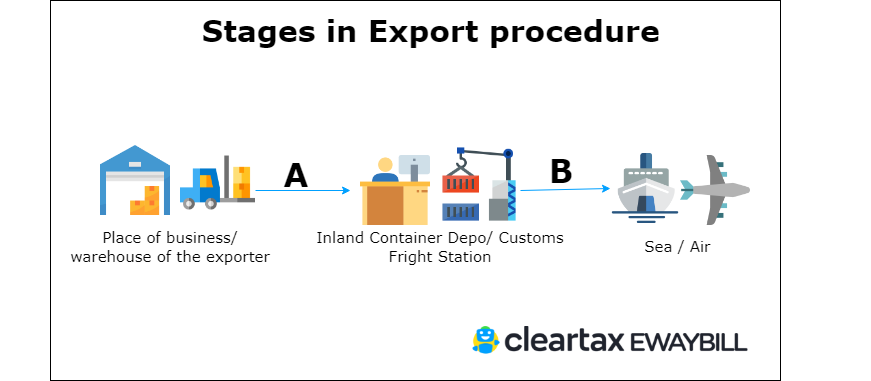

Stages in the Export procedure is as follows:

A- when goods are being transported from the place of business or warehouse of the exporter to an ICD/ CFS an e-way bill has to be generated.

B- transportation of goods from ICD/CFS to port is exempted from the requirement of carrying an e-way bill. Further, certain transactions are exempted from e-way bill requirement like petrol, diesel, kerosene, pearls etc. These exemptions hold good even for import and export transactions. Apart from these exemptions, specific movements are also exempted from e-way bill generation such as:

- Goods transported are transit cargo from or to Nepal/ Bhutan

- Movement of Goods between customs ports/station or between ICD/CFS and ports either under customs bond or under customs supervision or seal.

- A case of movement between customs area to ICD or vice versa as given under stage B in the below illustrations of Import and Export.

How to generate e-way bill for imports and exports?

The portal and the steps to generate the e-way bill remains same in case of import or export transaction. But below are some key points a user has to note while generating an e-way bill in this situation:

| Particulars in e-way bill | Import | Export |

| Transaction sub-type to select | Import | Export |

| Document type and number | Bill of entry | Tax invoice meant for export of goods |

| Bill From | Unregistered Person (URP) | Exporter's details (name, GSTIN etc.) |

| Dispatch From | Pin code 999999 has to be entered and in state column 'other countries' to be selected | Address of exporter's place of business/ warehouse |

| Bill to | Importer details (name, GSTIN etc.) | A person outside India who maybe unregistered (mention URP) |

| Ship to | Address of importer's place of business/ warehouse | Pin code 999999 has to be entered and in state column 'other countries' to be selected |

| Transportation details | Details of transporter (vehicle details, transporter ID etc.) | Details of transporter (vehicle details, transporter ID etc.) |

One of the key aspects of an e-way bill is to calculate the validity of an e-way bill based on the distance to be travelled. So when we have cases of import and export, we need to know from what point we need to start calculating the distance in order to know the validity.

a. In case of import, the e-way bill has to be generated once the goods are cleared for home consumption. The distance has to be calculated from the ICD to the place of business of the importer and validity of the e-way bill determined accordingly.

b. In case of export, the e-way bill has to be generated when the goods are being moved to the port for exportation. For e-way bill validity purpose, the distance will be calculated from the warehouse/ place of business to the port.

Is e-way bill required for high sea sales?

What happens when there is a high sea sale? Since the sale is not covered in any of the above illustrations and it takes place outside the boundaries of India, there is no need to generate an eway bill. Therefore, we can conclude that the government is making efforts to reduce the compliance burden for businessmen involved in foreign trade. If the importers and exporters ensure the other documents like shipping bill and bill of entry are in place and the e-way bill is valid, the process is surely going to be less cumbersome.

India's Fastest and Most Advanced 2B Matching

Maximise ITC claims, use smart validations to correct your data and complete 2B matching in <1 minute

How To Generate A Registered Bonded Bill Of Exchange

Source: https://cleartax.in/s/gst-eway-bill-import-export

Posted by: robertsgoodst.blogspot.com

0 Response to "How To Generate A Registered Bonded Bill Of Exchange"

Post a Comment